AI Infrastructure (Vector DBs & Model Hosting) Valuations: Q1 2026

AI infrastructure valuations in Q1 2026 are bifurcating sharply, with vector databases commanding 6 to 11x EV/Revenue and model hosting and inference platforms clearing 4 to 9x, as NRR above 120% and p95 latency under 20ms emerge as the defining criteria separating upper-quartile assets from the rest of the range. Pinecone's $750M-plus valuation and Hugging Face's $4.5B mark anchor the comparable set, while the projected expansion of the vector database market from $2.65B to $8.95B at a 27.5% CAGR through 2030 underscores the structural demand behind these multiples. The report covers subsector valuation methodology, compute efficiency benchmarks including H100 throughput exceeding 3,500 tokens per second under optimized batching, enterprise moat drivers such as SOC2 and VPC peering premiums, and the capital allocation shift toward inference infrastructure as 2026 marks the crossover point where inference spend overtakes training.

- Sector

- AI

- Focus

- Valuations

- Published

- January 15, 2026

- Length

- 22 slides

- Reading time

- 14 minutes

Key findings

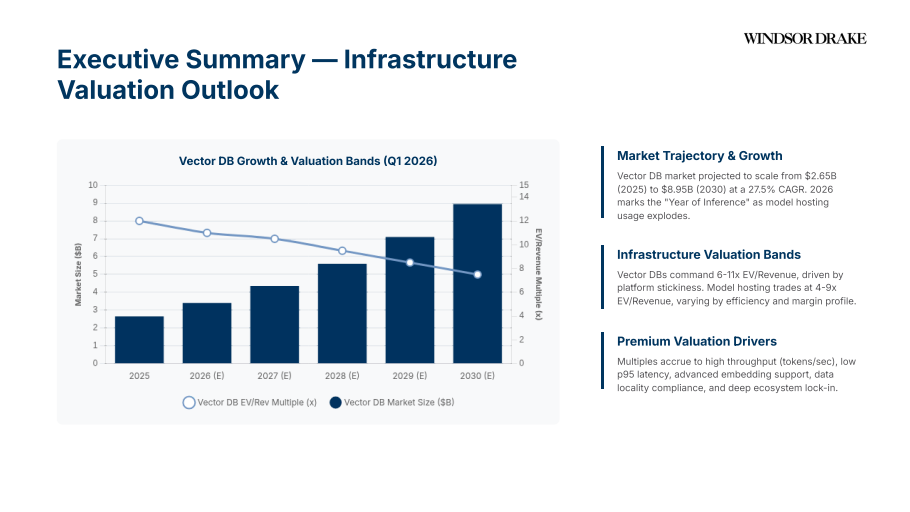

- The vector database market is projected to grow from $2.65B in 2025 to $8.95B in 2030 at a 27.5% CAGR, driven by RAG adoption and enterprise AI standardization.

- Vector databases command EV/Revenue multiples of 6–11x, while model hosting and inference platforms trade at 4–9x, with efficiency metrics as the primary differentiator.

- Pinecone carries a $750M+ valuation signal driven by serverless, consumption-based pricing and strong NRR; Hugging Face is valued at $4.5B reflecting platform lock-in potential.

- Replicate has raised $58M+ in funding and is gaining traction in image and video generation workloads, with gross margins improving via cold-boot optimizations.

- Spot instance arbitrage can deliver 60–80% compute cost savings, while INT8/INT4 quantization provides 2–4x memory reduction and roughly doubles throughput per GPU-hour.

- Top-tier H100 inference benchmarks exceed 3,500 tokens/sec using advanced batching (vLLM/TGI), versus a baseline of ~1,200, with optimized COGS of $0.15–$0.40 per 1M tokens.

- SOC2 and VPC peering capabilities command 20–30% pricing premiums, acting as high-barrier enterprise moats in financial and healthcare verticals.

- Platforms with services-heavy revenue (>30% mix), gross margins below 50%, or absent enterprise security features trade at lower-quartile multiples.

- Net Revenue Retention (NRR) above 120% is the key financial anchor for upper-quartile valuation; assets meeting this threshold alongside p95 latency under 20ms command premium multiples.

- 2026 marks the inflection point where inference spend overtakes training spend, shifting capital allocation toward efficient distributed serving infrastructure.

Methodology

This report synthesizes Windsor Drake's proprietary valuation framework with publicly available market data and industry signals current as of Q1 2026. Market sizing and CAGR projections for the vector database segment draw on third-party analyst forecasts, while compute benchmarking data references published performance figures for H100 GPU infrastructure and inference frameworks including vLLM and TGI. Valuation comparable ranges and EV/Revenue bands reflect Windsor Drake's calibration of disclosed funding rounds, secondary market signals, and observable pricing for companies including Pinecone, Hugging Face, Weaviate, Qdrant, Replicate, and Modal. No single third-party data provider is solely relied upon; Windsor Drake's contribution lies in the cross-category synthesis, valuation band construction, and strategic read-through for builders, buyers, and investors.

Frequently asked questions

What EV/Revenue multiples are AI infrastructure companies trading at in Q1 2026?

Vector databases currently command 6–11x EV/Revenue, reflecting their role as critical RAG infrastructure with high data gravity and enterprise stickiness. Model hosting and inference platforms trade at 4–9x EV/Revenue depending on throughput efficiency, developer velocity, and autoscaling capabilities. Observability and data ops tools trade at a comparable 6–10x range.

What drives premium valuations for vector database and model hosting companies?

Premium multiples accrue to platforms demonstrating p95 latency under 20ms, throughput above 3,500 tokens/sec on H100s, and Net Revenue Retention above 120%. Business-level drivers include enterprise SLA guarantees, data locality and sovereign cloud compliance, and deep ecosystem lock-in via integrations with frameworks like LangChain and LlamaIndex.

Who are the key players in the vector database market right now?

The leading vector database platforms as of Q1 2026 are Pinecone (managed-first serverless, $750M+ valuation signal), Weaviate (open-source plus cloud hybrid with BYOC and hybrid search), and Qdrant (Rust-based OSS engine emphasizing compute efficiency and high-throughput ingestion). The landscape is bifurcating between managed-first platforms commanding premium valuations and OSS cores driving developer adoption.

How does open-source versus managed model hosting affect valuation multiples?

Managed services such as those from OpenAI, Anthropic, and Cohere command higher multiples due to recurring revenue quality, high NRR, and sticky prompt-engineering workflows. Open-source models like Llama 3 and Mistral drive wider adoption funnels but monetize via enterprise add-ons such as RBAC, SSO, and support tiers, with valuation anchored on conversion rates from free-tier to paid seats.

What are the biggest cost levers and margin profiles for AI inference infrastructure?

Compute is the largest margin drag at 50–65% gross margin, while storage (65–75%) and network (70–80%) layers offer better profiles. Key efficiency levers include INT8/INT4 quantization for 2–4x memory reduction, batching and KV-caching, and spot instance arbitrage delivering 60–80% cost savings. Optimized PaaS infrastructure can target 50–65% gross margins versus 35–45% for base infrastructure resale.

What diligence priorities should buyers and investors focus on for AI infrastructure M&A in 2026?

Buyers should validate historical telemetry scale and SLO adherence, verify p95 latency and autoscaling behavior under real load, and scrutinize data governance and sovereign cloud capabilities. Financial diligence should stress-test TCO roadmaps against hardware deflation curves and confirm GPU supply contract flexibility to hedge against capacity shocks.

How large is the vector database market and what is its projected growth rate?

The vector database TAM is projected to grow from $2.65B in 2025 to $8.95B by 2030, representing a 27.5% CAGR. Primary growth catalysts include Retrieval-Augmented Generation (RAG) adoption, multimodal embedding use cases, serverless architectures lowering TCO, and enterprise data governance requirements driving demand for managed solutions.

Companies covered

Public and private companies referenced in this report.